Prices under emissions trading schemes have been low to date. Sometimes this may be because systems are new, but the EUETS is long established and needs to demonstrate that it can now produce adequate prices.

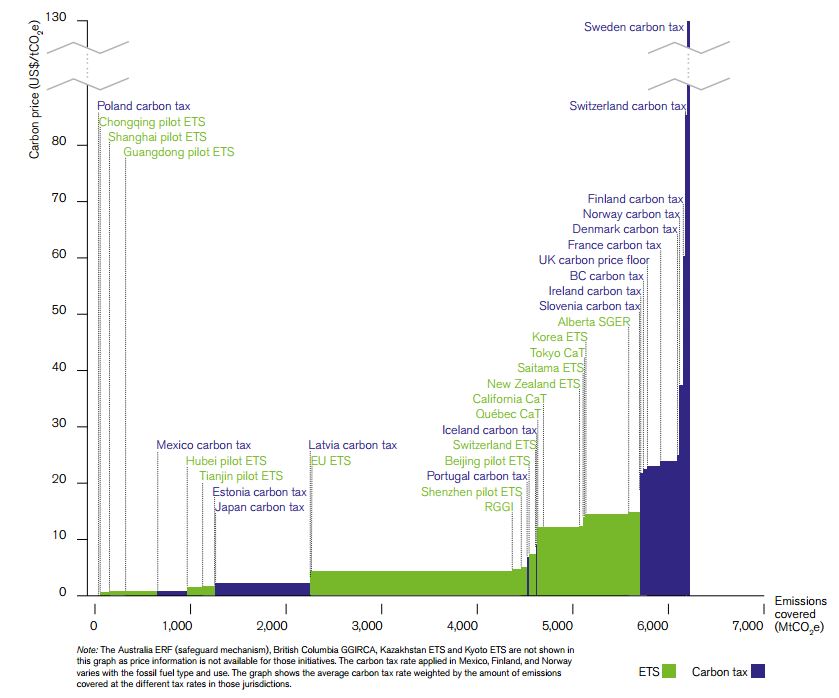

Prices under emissions trading systems around the world have so far remained low. The chart below shows carbon pricing systems arranged in order in increasing price, with prices on the vertical axis shown against the cumulative volume covered on the horizontal axis. Carbon taxes are shown in purple, emissions trading systems in green. It is striking that all of the higher prices are from carbon taxes, rather than emissions trading systems.

Prices under Emissions Trading Systems and Carbon taxes in 2016

Source: World Banks State and Trends of carbon pricing report[1]. Prices are from mid-2016.

Prices in the largest emissions trading system, the EUETS have been around $5-6/tonne, and prices in the Chinese pilot schemes have been similar and in some cases even lower, although with little trading. The price under the California and Quebec scheme (soon to be joined by Ontario) is somewhat higher. However, this is supported by a floor set in advance and implemented by an auction reserve price. If this price floor were not present a surplus of allowances would very likely have led to lower prices. The Korea scheme has had very low trading volumes, so does not provide the same sort of market signal found under more liquid schemes.

In contrast, a wide range of carbon taxes are already at higher levels and in some cases are due to increase further. The French carbon tax, which covers sectors of the economy falling outside the EUETS, is planned to reach €56/tCO2 (US$62/tCO2) in 2020 and €100/tCO2 (US$111/tCO2) in 2030[2]. In Canada a national lower limit on carbon prices for provinces with an explicit price-based system (not shown on the chart) is due to reach $50 per tonne in 2022[3]. The UK carbon price floor, which covers power sector emissions, was due to rise to substantially above current levels, but is currently being kept constant by the Government, mainly because the price under the EUETS is so low.

Increases such as those due in France and Canada will bring some carbon taxes more in line with the cost of damages, and thus to economically efficient prices. The cost of damages is conservatively estimated at around $50/tonne[4], rising over time (see here for a discussion of the social cost of carbon and associated issues). The increases will also bring prices more into line with the range widely considered to be necessary to stimulate adequate low carbon investment[5].

Low prices under emissions trading systems have been attributed to a range of factors, including slower than expected economic growth and falling costs of renewables[6]. However these factors do not explain the consistent pattern of low prices across a variety of systems over different times[7].

While it is difficult to derive firm evidence on why this pattern should be present, two factors seem plausible. The first is systematic bias in estimates – industry and governments will expect more growth that actually occurs, costs will be overestimated, and these tendencies will be reflected in early price modelling, which can often overstate likely prices.

But the second, more powerful, tendency appears, based on anecdotal evidence, to be that there is an asymmetry of political risk. The political costs of unexpectedly low prices are usually perceived as much less than those of unexpectedly high prices, and so there will always be tendency toward caution, which prevents tight caps, and so leads to prices being too low.

This tendency is difficult to counteract, and has several implications for future policy.

First, it further emphasises the value of price floors within emissions trading systems. Traditional environmental economics emphasises the importance of uncertainty around an expected level of abatement costs or damages. If decision makers are not in fact targeting expected average levels, but choosing projections of allowance demand above central expectations then the probability of very low prices is increased, and the case for the benefits of a price floor is stronger.

Second, it implies that it is even less appropriate than would anyway be the case to expect the carbon price alone to drive the transition to a low carbon economy. Measures so support low carbon investment, which would in any case be desirable, are all the more important if the carbon price is weak (see here for a fuller discussion of the value of a range of policy measures). While additional measures do risk further weakening the carbon price, they should also enable reduced emissions and tighter caps in future.

Third, it requires governments to learn over time. Some low prices may reflect the early stage of development of systems, starting slowly with the intention of generating higher prices over time. However this does require higher prices to eventually be realised.

The EUETS has by some distance the longest-established system, having begun eleven years ago and with legislation now underway for the cap to 2030, by which time the system will be 25 years old. The EU should be showing how schemes can be tightened over time to generate higher prices. However it now looks as though the Phase 4 cap will be undemanding compared with expectations (see previous posts). The recent vote by the European Parliament’s ENVI committee failed to adopt measure that are adequate to redressing the supply demand balance, with tweaks to the market stability reserve unlikely to be enough. This undermines the credibility of cap-and-trade systems more generally, rather than setting the example that it should. Further reform is needed, including further adjustments to supply and preferably auction reserve prices.

The advantages of cap-and trade systems remain. Quantity limits are in line with the international architecture set by the Paris Agreement. They also provide a clear strategic signal that emissions need to be reduced over time.

However there is little evidence to date that emissions trading systems can produce adequate prices. The EU, with by far the most experience of running an ETS, should be taking the lead in substantially strengthening its system. At the moment this leadership is lacking. Wider efforts to tackle climate change are suffering as a result.

Adam Whitmore – 23rd January 2017

[1] https://openknowledge.worldbank.org/handle/10986/25160

[2] World Bank State and Trends in Carbon Pricing 2016. See link in reference 1.

[3] http://news.gc.ca/web/article-en.do?nid=1132169 Canadian provinces with volume based schemes such as Quebec with its ETS must achieve emissions reductions equivalent to these prices.

[4] $40/tonne in $2007, see https://www.epa.gov/climatechange/social-cost-carbon, escalated to about $50 today’s dollars.

[5] See this recent discussion: https://www.weforum.org/events/world-economic-forum-annual-meeting-2017/sessions/the-return-of-carbon-markets

[6] Ref: Tvinnereim (2014) http://link.springer.com/article/10.1007%2Fs10584-014-1282-1#page-1

[7] The South Korea ETS may be a partial exception to the pattern. However it is unclear due to the lack of liquidity in the market.